The missing middle

Calling all those intermediaries, your time has come.

[As I travel home from London, I was tempted to call this “Mind the gap.”]

In August of 2022, I wrote a short post called New horizons, new horizontals. The purpose of this post was to present a reasonable, if abbreviated, playbook for modern, new space constellations. I have wanted to return to this post for some time because there is a key factor that I did not expand on the missing middle.

We have discussed the idea of complementary assets frequently on Strategic Geospatial. In essence, we mean those technologies or processes that enable new geospatial capabilities. “The cloud” is a good example. Though the cloud is not explicitly geospatial, cloud technology enables modern, highly scalable geospatial activities. Indeed, the cloud enables the distribution of massive amounts of remote sensing data. The cloud is, therefore, a complementary asset for Modern Geospatial practices.

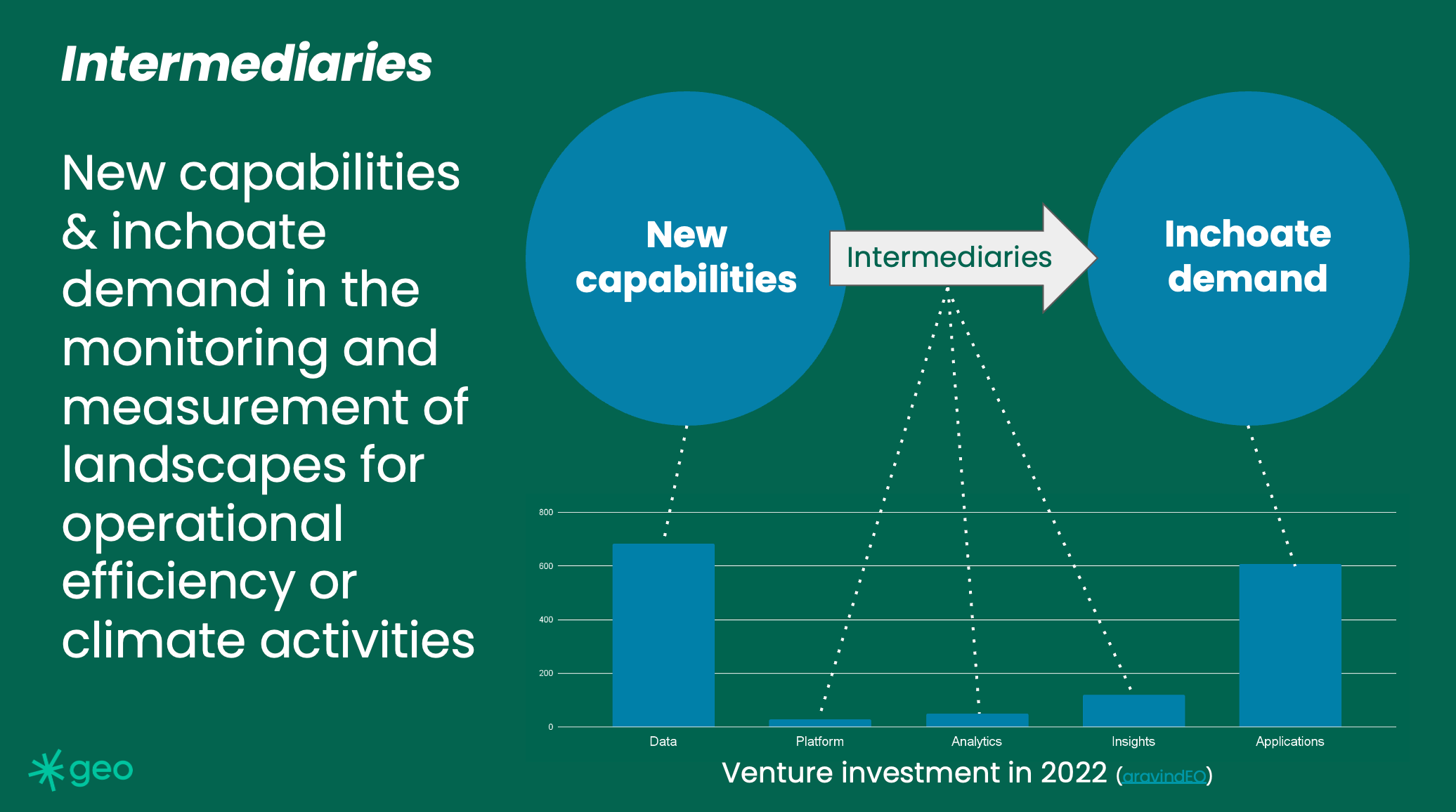

The growth and combination of several complementary assets have created a series of new capabilities I call “Modern Geospatial” for convenience. These capabilities offer the market an opportunity to understand the changing surface of our planet and human activities at a scale and granularity never before seen. These are net-new capabilities.

On the far side of this equation is an inchoate demand. This is an unclear or unmet need. But this need is not explicit. Climate is an example. We know that “climate” is a problem; we know that landscape change will have to be measured to measure this problem in some way. So, modern geospatial will be part of the equation. But we have no idea what products will eventually serve this market; we don’t even know what questions the market will need to answer. I've used this word "inchoate" before on Strategic Geospatial, but it is unusual. That said, I haven't found a better, simpler one.

So, we have new capabilities on one side of our market equation, and we have a demand (of sorts) on the other side. But in the middle, our market is missing something; there are few intermediaries*. Why not?

With thanks to Aravind Ravichandran for the venture investment numbers, we can see a general lack of investment into intermediaries. But, if we use our foresight, we can see that, at some point, analytics of landscape change will power many decision-making processes. I say this not out of an abundance of optimism but from a position of practicality. The capabilities already exist, and more sensory capacity is launched weekly. As our populations grow, increasing pressures on our landscape will demand better decision-making data. The most scalable data source presently available is satellite-based. I would argue that Earth observation-derived geospatial analytics are an inevitability, but I would hazard that observation with the fact that I have no idea of timing.

And timing is probably the most important factor.

So, what is limiting or impacting the timing? Several supply factors need to converge to enable this market:

Access to data - data must be available in open or industry standards, APIs, programmatic search

Pricing of data - data for commercial applications needs to be cheap

Enough data - ironically, though there is a lot more data available, there still isn't enough to meet market expectations

Fusion of data - no single constellation will answer a question, we will have to become very good at data fusion

And, there are a few demand factors too:

Knowledge of data - consumers must know that Earth observation data is an option.

Knowledge of what to do with the data - consumers need to be better at using pixels or have the pixel abstracted away

Identification of opportunities - consumers need to know what is possible by interpreting spectra and space with imagery.

You can imagine these lists each as a cycle, each of which ultimately keeps repeating. Perhaps you could even see these as a sort of double helix because supply and demand are intertwined. As a geospatial community, we need both the supply and demand to develop together. Today, I would argue they have fallen out of step, which may be the reason for the missing middle. Critically, the demand side has not ramped up.

I would argue that the demand side had looked much perkier immediately before Russia invaded Ukraine in 2022. Debates around carbon and climate were demanding EO solutions. Then they stopped in an energy crisis. We can argue the logic of this reaction, but that was the net effect I saw. Since then, the commercial demand has waned. However, observing the seemingly credible efforts and announcements from COP28, perhaps we will see a resurgence again.

But climate will not be the only market. I see a future where any land-oriented activity will have an EO-based data feed. There will be golf course condition apps, real estate climate score apps, road condition apps, automotive supply chain apps, fire fuel risk apps, and solar roof apps. Most of these things probably exist in some form already, but a good sign will be when a market emerges - that there is more than one competing for their segment. Each team will have their specialist EO engineers and domain experts creating specialist analytics. One great example of this today is Earth-i, creating steel supply chain analytics, without a map in sight.

Because pixels are an awkward, reflective representation of our planet, without specialists those intermediaries are hard businesses to create. Each one of them needs our community's support and good wishes. Stepping into the arena is always fearsome, more so in a nascent market, but the benefits of winning could be out of this world.

*As soon as I say this, I will be inundated with examples of good intermediaries. There are a number, but there are clearly not enough. That said, do feel free to share new and interesting examples with me.

Great article! From my perspective, the overall lack of consumer understanding cross the board (summarizing the key demand factors) is the single biggest inhibitor to industry growth. As an industry, we have to do better to educate the masses on the value of the data (EO, SAR, IR, RF, etc.) and the derivative insights.

New intermediaries to pay attention to: Messium, GenMat, FourPoint

Thank you Will. Your article is valuable in not only highlighting the issue/opportunity, but in pointing to a key solution factor (to identifying new and meaningful intermediaries)...which is to ramp-up and multiply methods of engagement within the community. Strategic Geospatial and North51 are excellent examples...but what more can we do to catalyze and diversify the conversation?